{kind=link}

What if your retirement portfolio is betting on the wrong people, not the right demographics?

Demographic shifts like population aging, falling fertility, longer life spans and migration move slowly but reshape growth, savings, and demand over decades.

Those slow forces change expected returns, the need for stable income, and which sectors outperform.

This post lays out the transmission channels: life-cycle saving, cohort size, and consumption composition.

It then maps those channels into practical allocation moves for retirement portfolios.

You’ll get watchpoints and clear tilts to consider now.

Core Ways Demographic Trends Shape Long‑Term Asset Allocation Decisions

Understanding how demographic trends affect long‑term asset allocation starts with population aging, shifting fertility rates, and migration flows. These are foundational structural forces that reshape economies and markets over decades. Unlike interest rates or inflation, which can swing quarterly, demographics move slowly, decade by decade. But their cumulative effect determines trend growth, government finances, and the structural balance between savers and spenders. Population aging describes the rising share of retirees relative to workers, raising the old‑age dependency ratio and shifting aggregate demand from capital accumulation to capital preservation while placing fiscal pressure on social safety nets.

These forces work through three primary channels. First, life‑cycle saving: younger cohorts accumulate financial assets while older cohorts spend down or shift toward income‑generating instruments, changing net flows into equities, bonds, and real estate. Second, cohort size: large generational waves create sustained demand surges and troughs for housing, healthcare, and financial services as they move through age brackets. Third, consumption composition: older households spend proportionately more on healthcare, less on discretionary goods, and prioritize stable income, shaping sector performance and factor returns over multi‑decade horizons.

A framework linking demographics to portfolio design starts with three questions: What’s the prevailing direction of national or regional savings behavior? What does the age structure imply for GDP growth and productivity trends? How will cohort composition affect household risk appetite and income needs? Answering these lets you map demographic forecasts onto strategic asset allocation, adjusting for expected real returns, changes in equity risk premia, and evolving income requirements tied to life expectancy and retirement planning.

The global population aged 65+ stands above 10 percent today and is projected to reach roughly 25 percent by 2100. It’s a structural shift already visible in advanced economies where dependency ratios are rising sharply. The EU old‑age dependency ratio is forecast to climb from approximately 33 percent in 2022 to 60 percent by 2100. Japan’s ratio may approach 80 retirees per 100 workers by mid‑century. These projections translate into broad strategic‑allocation principles: longer investment horizons must account for lower trend growth, higher structural demand for safe income, rising healthcare and aged‑care expenditure, and pronounced geographic divergence in growth opportunities.

Major Demographic Forces Investors Must Track for Asset Allocation

Fertility rate changes begin with the observation that most developed nations now record total fertility rates below the replacement level of 2.1 children per woman. The United States fell below 1.6 in 2024. This implies shrinking cohorts of working‑age individuals absent offsetting migration. Lower fertility translates directly into slower labor‑force growth, reducing the numerator in the simple GDP identity: GDP equals the number of workers multiplied by productivity per worker. When fewer workers enter the economy, sustaining growth requires either higher productivity or an expansion of the workforce through immigration.

Migration dynamics shape labor supply, wage inflation, and aggregate demand in receiving economies. Countries with positive net migration can partially offset aging pressures by adding younger workers who contribute tax revenues, support housing demand, and increase consumption. Regions with restrictive migration policies or net emigration face accelerated dependency‑ratio increases and heightened fiscal strain. For investors, tracking annual net migration rates and policy signals provides early warnings of diverging growth paths and allows tactical geographic reallocation toward markets where labor‑force growth remains robust.

Life expectancy increases have added roughly eight years to global averages between 1990 and 2019. This extends required retirement savings horizons and amplifies the importance of longevity risk management. A retiree entering retirement at age 65 in 2024 may need to fund 25 to 30 years of spending, compared with 15 to 20 years a generation earlier. That raises the stakes for sequence‑of‑returns risk, inflation protection, and sustainable withdrawal rates. Longer lifespans also shift household preferences toward income stability and capital preservation earlier in the retirement transition, influencing demand for fixed income, dividend equities, and annuities.

Generational cohort investing recognizes that different age cohorts exhibit distinct financial behaviors shaped by their size, economic experiences, and lifecycle stage. Baby boomers have been the dominant force since 2010 as this large cohort began reaching age 65. By 2024 Boomers are roughly 60 to 78 years old, with peak retirement flows still underway through 2030. Millennials are now equally important: born 1981 through 1996, they’re approximately 28 to 43 years old in 2024, entering peak earning, household formation, and savings years. This creates sustained demand for housing, education funding, and retirement accounts. Generation Z, following Millennials, will begin entering prime working years in the late 2020s and early 2030s, shaping labor‑force and consumption trends into mid‑century.

Four key metrics form the core monitoring set for demographic‑aware allocation:

Fertility rate: births per woman. Levels below 2.1 signal future workforce contraction.

Net migration rate: annual arrivals minus departures per 1,000 population. Positive rates offset aging.

Median age: the age dividing the population into equal halves. Rising medians indicate aging societies. Australia’s median climbed from roughly 33 in the mid‑1990s to roughly 38 today, projected to reach the mid‑40s by the 2060s.

Old‑age dependency ratio (OADR): population aged 65+ divided by population aged 15 to 64, expressed as a percentage. Higher ratios imply fewer workers supporting each retiree.

Economic Transmission Channels Linking Demographics to Long‑Term Asset Returns

Savings rate trends and the balance between aggregate saving and investment determine equilibrium real interest rates and, by extension, the discount rates applied to all financial assets. Aging populations initially raise aggregate savings as large cohorts enter peak earning years. But once those cohorts retire they shift from net saving to net dissaving, drawing down financial assets to fund consumption. This lifecycle pattern has been observed in OECD economies where rising shares of retirees have coincided with sustained downward pressure on real rates, as the pool of patient savers seeking safe income grows while productive investment opportunities tied to labor‑force growth shrink. The result is structurally lower real risk‑free rates and compressed term premia, shaping long‑term bond yields and influencing equity valuations through lower discount rates.

Productivity and population structure interact to determine GDP growth and wage‑inflation dynamics. Slower labor‑force growth reduces potential GDP growth unless offset by higher productivity per worker. When labor becomes scarce, wage inflation can rise, compressing profit margins unless firms invest in automation, technology, or process improvements. OECD and ECB research flags that aging correlates with slower trend GDP growth. Absent policy intervention like delayed retirement, higher immigration, or productivity‑boosting reforms, you get prolonged low‑growth, low‑inflation regimes reminiscent of Japan’s experience since the 1990s. For capital markets, slower GDP growth tends to dampen nominal revenue growth for domestically focused firms and shifts investor preference toward companies with global revenue bases or exposure to productivity‑enhancing technologies.

Consumption patterns by age cohort create persistent sector and factor tilts as populations age. Younger households allocate higher shares of income to housing, education, transportation, and discretionary consumer goods. Middle‑aged households peak in overall spending and savings. Older households reduce discretionary outlays, increase healthcare and pharmaceutical expenditure, and prioritize stable income over capital gains. As the share of retirees rises, aggregate consumption tilts toward healthcare services, pharmaceuticals, medical devices, senior housing, leisure suited to older consumers, and financial services focused on wealth preservation and estate planning. These shifts translate into multi‑decade tailwinds for healthcare and staples sectors and headwinds for sectors tied to household formation or youth‑oriented discretionary spending.

Historical Lessons Showing How Demographics Influence Asset Allocation

Japan’s Nikkei 225 peaked at 38,915 on December 29, 1989. The subsequent three decades of equity market stagnation and persistently near‑zero government bond yields illustrate the capital‑market implications of aging without offsetting productivity or migration. Japan entered advanced aging earlier than other OECD nations, with its old‑age dependency ratio rising sharply through the 1990s and 2000s. The combination of a shrinking working‑age population, low productivity growth, and deflationary pressures kept nominal GDP growth near zero and compressed equity valuations. Japanese 10‑year government bond yields remained below 1 percent for most of the past two decades, driven by high domestic savings concentrated in aging households seeking safe income and by Bank of Japan policy accommodation. Japan demonstrates that demographic headwinds can override cyclical recoveries and sustain low‑return regimes across both equities and nominal bonds for extended periods.

The baby boomers retirement impact in the United States has unfolded more gradually but with equally significant market effects. As Boomers began retiring around 2010, aggregate household demand shifted from accumulation to preservation, supporting flows into fixed income, dividend‑paying equities, and target‑date funds. The surge in retirement accounts and defined‑contribution plan assets over the 1990s and 2000s coincided with Boomer peak earning years, driving strong equity inflows and contributing to valuation multiples. Now, as Boomers move through their 70s, they’re drawing down portfolios, creating structural demand for income‑generating assets and placing upward pressure on equity risk premia as the pool of incremental equity buyers shrinks relative to sellers.

Emerging markets with young populations have historically delivered stronger earnings growth compared to aging advanced economies. Countries such as India, Vietnam, and parts of Latin America maintain fertility rates above replacement and possess large cohorts entering working age, expanding labor supply, household formation, and consumption. These dynamics support higher nominal GDP growth, rising corporate revenues, and long‑term equity appreciation, provided political and institutional frameworks remain stable. For long‑horizon allocators, the demographic divergence between aging developed markets and younger emerging markets creates a structural case for geographic diversification, capturing growth tied to expanding workforces and rising per‑capita incomes in markets where dependency ratios remain low.

Asset Allocation Adjustments Driven by Demographic Trends

Asset Allocation Secrets: The Impact of Shifting Demographics provides detailed sector and asset‑class frameworks. The following subsections synthesize those insights into actionable allocation guidance.

Fixed Income Under Aging Demographics

Aging increases structural long‑term bond demand as retirees and near‑retirees shift portfolios toward income and capital preservation, reducing equity allocations and extending duration to match spending horizons that now stretch 25 to 30 years. Higher demand for sovereign bonds, investment‑grade credit, and inflation‑linked securities supports bond prices and compresses yields, particularly at the long end of the curve where retirees seek to lock in income. OECD and ECB research confirms that rising dependency ratios correlate with downward pressure on real interest rates, creating a structural tailwind for duration strategies and making high‑quality fixed income a core holding in portfolios exposed to aging demographics.

For tactical implementation, investors in aging markets should consider increasing fixed income allocations by 5 to 15 percentage points relative to historical norms, depending on liability profiles and risk tolerance. Laddered bond portfolios, long‑duration sovereign exposure, and inflation‑linked bonds provide protection against longevity risk and sequence‑of‑returns risk during the critical early years of retirement. Duration must be actively managed: while longer duration offers higher income and capital‑gains potential if yields fall further, it also exposes portfolios to mark‑to‑market losses if policy shifts or inflation surprises push yields higher. Scenario testing across rate environments helps calibrate duration targets to demographic and macro conditions.

Equity Market Sector & Factor Implications

Demographics raise the equity risk premium over long horizons by reducing the pool of net equity buyers and by compressing GDP growth expectations in aging economies. Empirical studies find that higher old‑age dependency ratios correlate with lower equity valuations and higher required returns, creating a structural headwind for broad equity indices in markets where working‑age populations are shrinking. But equity market sector rotation driven by aging creates pronounced winners and losers within the equity universe, allowing active allocators to capture demographic tailwinds by tilting toward favored sectors.

Healthcare spending stands out as the clearest demographic beneficiary: aging cohorts consume disproportionately more healthcare services, pharmaceuticals, medical devices, and long‑term care. Sector allocations that overweight healthcare by 5 to 15 percent versus market‑cap benchmarks capture this structural demand shift. Income‑oriented equities like dividend aristocrats, utilities, and real estate investment trusts focused on residential or healthcare properties also benefit as retirees prioritize yield over capital appreciation. Conversely, cyclical sectors tied to household formation and youth‑oriented discretionary consumer goods face weaker secular demand in aging markets.

Factor performance also shifts: value and quality factors tend to outperform growth and momentum in low‑growth, low‑rate aging regimes, as investors pay lower multiples for scarce earnings growth and prioritize balance‑sheet strength and dividend sustainability. Geographic and thematic diversification allows portfolios to balance domestic aging headwinds with growth opportunities elsewhere. Increasing exposure to younger emerging markets, automation and robotics sectors that offset labor scarcity, and global healthcare innovators helps.

Real Estate Demand Across Age Structures

Real estate demand exhibits mixed outcomes depending on age composition, migration trends, and property typology. Aging populations support demand for senior housing, assisted‑living facilities, age‑friendly apartments, and smaller dwellings suited to downsizing retirees. Regions with rising shares of residents aged 65+ see sustained demand for healthcare‑adjacent real estate and properties located in well‑serviced, walkable neighborhoods. These segments offer defensive cash flows and alignment with long‑term demographic shifts, making senior‑housing REITs, healthcare real estate funds, and private real estate allocations to age‑appropriate property types attractive holdings.

Conversely, real estate demand in regions experiencing shrinking working‑age populations faces structural headwinds: fewer young households reduce demand for new single‑family homes, while central‑business‑district office space suffers if remote work and population decline reduce office employment. Residential property markets in cities with net out‑migration or stagnant labor‑force growth may see weaker price appreciation and rising vacancy rates. For real estate allocations, geographic and typology selection is critical. Overweight age‑friendly, well‑located residential and healthcare properties in stable or growing regions. Underweight or avoid broad exposure to markets with severe projected labor‑force declines unless offset by strong migration or policy support.

| Asset Class | Demographic Impact | Portfolio Implication |

|---|---|---|

| Fixed Income (sovereign, IG credit) | Rising structural demand from retirees; downward pressure on real yields | Increase allocation +5–15pp; extend duration to match liabilities |

| Equities (broad) | Higher equity risk premium; slower GDP growth in aging markets | Tilt toward healthcare, dividends, quality; add EM exposure for growth |

| Real Estate (residential, senior housing) | Demand shift to age‑friendly properties; weakness in shrinking labor markets | Overweight senior housing REITs, well‑located residential; underweight CBD office in aging regions |

| Alternatives (infrastructure, private credit) | Stable cash flows attractive to retirees; illiquidity premium | Increase allocation +5–15pp for institutional/long‑horizon investors |

Geographic Allocation Effects of Global Demographic Divergence

Global aging and cross‑border allocation strategies must account for pronounced divergence in demographic trajectories across regions. Europe faces severe fiscal pressure as old‑age dependency ratios climb toward 60 percent by 2100, forcing governments to choose between higher taxes, reduced social benefits, or increased public debt. Japan and South Korea exhibit the most advanced aging, with Japan’s dependency ratio potentially reaching 80 retirees per 100 workers by mid‑century and Korea’s median age already in the mid‑40s. This creates persistent low‑growth, low‑rate environments and structural headwinds for domestic equities absent productivity breakthroughs or policy reforms. In contrast, the United States experiences slower aging due to relatively higher immigration and a larger Millennial cohort now entering peak earning years, supporting continued demand for income assets but retaining more growth orientation than Europe or East Asia.

Emerging markets offer the starkest geographic contrast: countries such as India, Vietnam, Indonesia, and parts of sub‑Saharan Africa maintain young populations with median ages in the 20s or low 30s and dependency ratios well below 20 percent. These markets benefit from expanding labor forces, rising household formation, and consumption growth, creating a multi‑decade tailwind for equities, real estate, and local‑currency fixed income. Country allocation based on demographics suggests overweighting younger emerging markets by 5 to 15 percent versus standard benchmarks, capturing the demographic dividend as working‑age populations grow and per‑capita incomes rise.

Migration policy and capital flows act as critical differentiators within both developed and emerging markets. Australia mitigates domestic aging pressures through sustained positive net migration, maintaining labor‑force growth and housing demand despite a rising median age. Canada pursues similar strategies. Countries with restrictive immigration policies or net emigration face accelerated dependency‑ratio increases and weaker long‑term growth prospects. Monitoring annual migration data, policy announcements, and demographic projections allows tactical reallocation toward markets where migration offsets aging and away from regions where labor‑force contraction is accelerating unchecked.

Portfolio Construction Framework Incorporating Demographic Forecasts

Integrating demographic data into strategic asset allocation requires a systematic approach that tracks leading indicators, models multiple scenarios, and adjusts allocation bands and glidepaths in response to observed and projected demographic shifts. Unlike cyclical macro variables, demographics move predictably. Birth cohorts today determine the workforce 20 years hence. This allows long‑horizon investors to anticipate structural changes and position portfolios ahead of consensus.

Six core demographic metrics to track quarterly or annually:

Share of population aged 65+: rising shares signal increased demand for income, healthcare, and capital preservation.

Old‑age dependency ratio: percentage of population 65+ relative to working‑age population (15–64). Values above 30 percent indicate material fiscal and growth pressures.

Median age: populations with median ages above 40 face near‑term aging headwinds. Below 30 suggests demographic tailwinds.

Fertility rate: sustained rates below 2.0 children per woman forecast future workforce contraction.

Net migration rate: positive rates (above +2 per 1,000) offset aging. Negative rates accelerate it.

Labor‑force participation rate: tracks the active workforce share. Declining participation among prime‑age workers compounds aging effects.

Scenario Modelling Steps

Scenario analysis structures demographic uncertainty into three cases: mild aging, moderate aging, and severe aging, each mapped to quantitative assumptions for GDP growth, real interest rates, and equity risk premia. A mild aging scenario assumes fertility stabilizes near 1.8, positive net migration, and modest dependency‑ratio increases. GDP growth slows by 0.0 to 0.2 percentage points per decade, real risk‑free rates decline by 0.25 percent over ten years, and equity risk premia rise by 50 basis points. Portfolio implications are modest: slight overweight to fixed income, modest healthcare tilt, maintain growth exposure.

A moderate aging scenario projects fertility remaining below 1.6, flat or slightly negative net migration, and dependency ratios rising by 5 to 10 percentage points over a decade. GDP growth deceleration of 0.2 to 0.4 percentage points per decade, real rates falling 0.5 to 0.75 percent, and equity risk premia lifting 100 to 150 basis points. Allocation shifts include increasing fixed income by 10 percentage points, raising healthcare and dividend‑equity exposure by 10 to 15 percent, adding 5 to 10 percent emerging‑market equities for growth, and incorporating inflation‑linked bonds for longevity protection.

A severe aging scenario assumes fertility below 1.4, net emigration or zero migration, dependency ratios climbing 10+ percentage points, and no offsetting productivity gains. GDP growth reduction of 0.4 to 0.5 percentage points per decade, real rates dropping 0.75 to 1.0 percent, and equity risk premia expanding 150 to 200 basis points. Strategic responses include increasing fixed income to 60+ percent of portfolios, heavy overweights to healthcare and defensive sectors, material allocations to younger emerging markets (15+ percent), substantial duration extension, and inclusion of alternatives (infrastructure, private credit) for stable cash flows. Regular stress tests across these scenarios help investors understand sensitivity to demographic assumptions and identify allocation adjustments that improve resilience across outcomes.

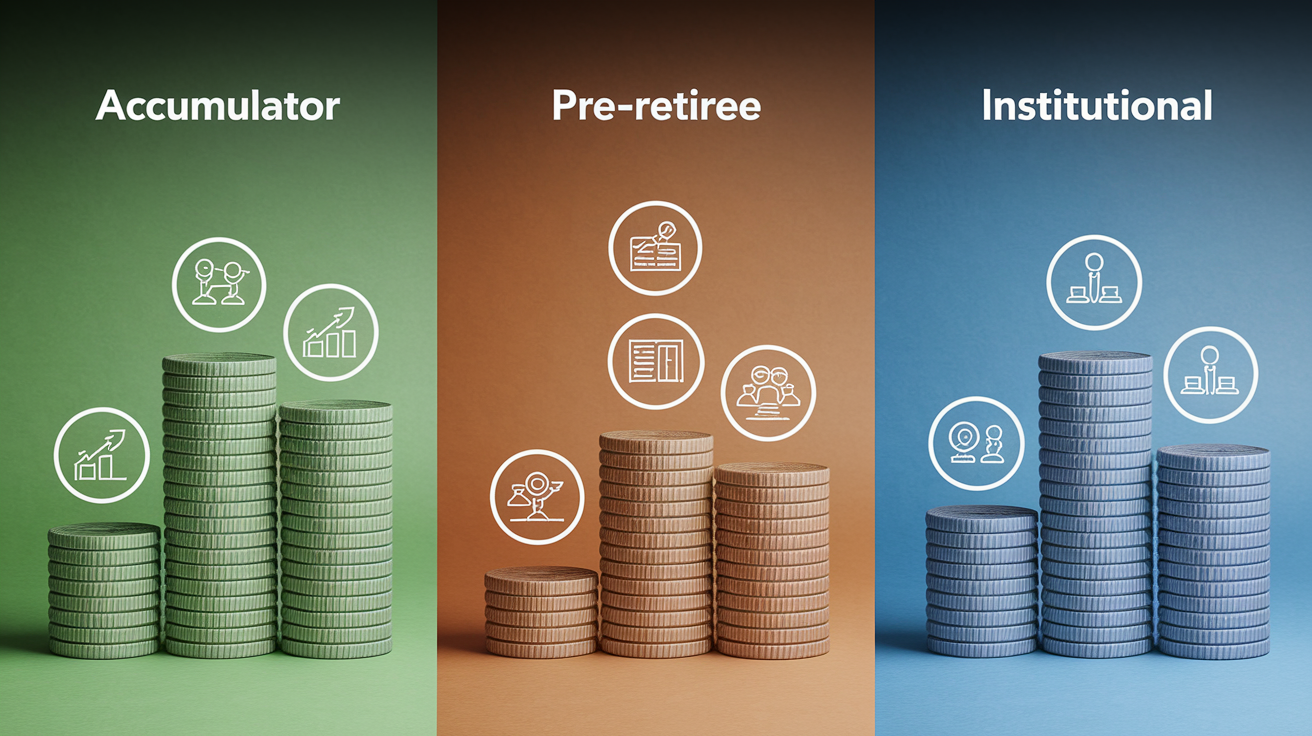

Sample Asset Allocation Adjustments for Different Investor Profiles Under Demographic Change

Lifecycle funds and age targeting incorporate demographic trends by adjusting strategic allocations as investors progress through accumulation, pre‑retirement, and retirement phases, with each phase exhibiting distinct saving behavior, risk capacity, and income needs shaped by broader cohort dynamics.

Accumulator (age <40, long horizon): equities 70 to 85 percent, bonds 10 to 25 percent, alternatives 5 to 10 percent. Overweight emerging‑market equities by 5 to 10 percent to capture demographic dividends in younger populations. Tilt within equities toward technology, automation, and global healthcare to benefit from productivity and aging‑linked secular growth. Accept higher volatility in exchange for compounding returns over multi‑decade horizons. Maintain minimal fixed income except for liquidity and rebalancing reserves.

Pre‑retiree (age 45–59, transition phase): equities 50 to 65 percent, bonds 25 to 40 percent, alternatives 5 to 15 percent. Begin shifting toward income‑generating assets. Add dividend‑paying equities, increase allocation to investment‑grade fixed income and inflation‑linked bonds by 5 to 15 percentage points, and introduce senior‑housing or healthcare REITs. Reduce cyclical equity exposure and raise healthcare, utilities, and quality‑factor tilts by 5 to 10 percent. Extend fixed income duration to begin matching anticipated retirement spending horizon. Build 1 to 2 years of cash or short‑duration reserves to reduce sequence‑of‑returns risk as retirement approaches.

Retiree (age 60+, decumulation phase): equities 30 to 50 percent, bonds 35 to 60 percent, alternatives 5 to 20 percent. Prioritize capital preservation and stable income: increase high‑quality sovereign and corporate bonds, dividend aristocrats, and inflation protection. Maintain 3 to 5 years of anticipated spending in cash, money‑market funds, or short‑duration bonds to avoid forced asset sales during market downturns. Equity allocation focuses on healthcare, utilities, consumer staples, and global dividend payers. Reduce or eliminate exposure to cyclicals, small‑cap growth, and sectors sensitive to household formation. Consider annuities or other longevity‑hedging instruments if life expectancy and retirement planning horizons exceed 25 years.

Institutional (pension, endowment, insurance): tailor allocations to liability duration and demographic profile of beneficiaries. Increase inflation‑linked bonds and long‑duration fixed income to match multi‑decade liabilities. Add 5 to 15 percent allocations to private infrastructure, healthcare real assets, and private credit to capture illiquidity premia and demographic‑driven cash flows. Overweight sectors and geographies aligned with aging (healthcare, senior housing, automation) and younger demographics (emerging‑market equities, consumer growth in India and Southeast Asia). Implement liability driven investment strategies that dynamically hedge interest‑rate and longevity risk, rebalancing as dependency ratios and cohort compositions evolve.

Tools, Monitoring Cadence, and Risk Management for Demography‑Driven Allocations

Portfolio rebalancing frequency for demographic‑aware allocations should align with the pace of demographic data releases and the materiality of observed changes. Core demographic indicators are typically updated annually by national statistical agencies and supranational bodies (United Nations, OECD, World Bank), making an annual review cadence appropriate for strategic asset allocation adjustments. However, investors should establish quantitative triggers that prompt interim rebalancing: a dependency‑ratio change of 2 percentage points or more, cohort‑size forecast shifts exceeding 5 percent over a five‑year window, or abrupt migration‑policy changes that materially alter labor‑force projections.

Key risk considerations include concentration risk from over‑tilting to aging‑winner sectors without maintaining adequate diversification across geographies, sectors, and factors. Excessive healthcare or defensive exposure can underperform during cyclical recoveries or productivity booms, requiring periodic rebalancing back to strategic targets. Policy risk is equally important: fiscal responses to aging can rapidly shift the demographic‑economic linkage, making sensitivity analysis and scenario planning essential components of ongoing risk management. Inflation risk and longevity risk interact in complex ways. Stress testing portfolios for longevity helps ensure adequate growth and inflation protection remain in place despite tilts toward income and preservation.

Five monitoring items for demographic‑driven portfolios:

Quarterly review: track updated dependency ratios, migration flows, and labor‑force participation. Compare actuals to forecasts and adjust if deviations exceed 1 percentage point annually.

Annual strategic review: update demographic scenarios (mild/moderate/severe aging), refresh long‑term return assumptions for asset classes and sectors, and rebalance allocations if strategic bands are breached.

Policy surveillance: monitor legislative changes (retirement age, immigration quotas, social‑security reforms) and central‑bank commentary on demographic effects. Material policy shifts warrant interim allocation reviews.

Thematic strategy rebalancing: for targeted exposures (robotics, automation, healthcare innovation), follow the strategy’s cadence. Some thematic funds rebalance monthly to maintain exposure to leading innovators and manage turnover.

Stress testing: run tri‑annual or annual stress tests across demographic scenarios, interest‑rate shocks, inflation surprises, and longevity extensions. Ensure portfolios remain resilient to adverse combinations (severe aging plus high inflation, for example) and maintain sufficient liquidity and diversification to weather multi‑year drawdowns.

Final Words

In the action: slow-moving forces: aging populations, fertility declines, and migration are already shifting saving, consumption, and workforce size. This piece mapped the channels, historical lessons, and a framework linking cohort behavior to strategic allocation.

Near term: watch dependency ratios, median age, migration flows, and life expectancy. Use mild, moderate, and severe aging scenarios to stress-test glidepaths and liabilities.

Apply these signals to rebalance with intent. Understanding how demographic trends affect long-term asset allocation makes portfolios more resilient and positions you to capture the longer-run opportunities ahead.

FAQ

Q: How do demographic trends affect long-term asset allocation?

A: Demographic trends affect long‑term asset allocation by shifting saving and spending patterns, real‑rate pressures, and growth expectations—so tilt strategic weights toward assets that match longer savings horizons and lower growth scenarios.

Q: What are the main demographic forces investors should track?

A: The main demographic forces investors should track are population aging, fertility declines, migration flows, and changing life expectancy, because each alters workforce size, consumption mix, and aggregate saving behavior.

Q: Which metrics best indicate demographic risk for portfolios?

A: The metrics that best indicate demographic risk for portfolios are fertility rate, net migration, median age, old‑age dependency ratio, share 65+, and cohort size changes over five‑ to ten‑year horizons.

Q: How do aging populations change macroeconomic returns and interest rates?

A: Aging populations change macro returns and interest rates by raising savings demand, lowering trend GDP growth, and putting downward pressure on real rates, which lifts required equity premia and duration sensitivity.

Q: What historical examples show demographics influencing markets?

A: Historical examples showing demographics influencing markets include Japan’s post‑1989 stagnation linked to extreme aging and emerging markets’ faster earnings growth during demographic dividends when working‑age populations expanded.

Q: How should strategic allocation change under aging demographics?

A: Strategic allocation should change under aging demographics by increasing emphasis on income stability, duration management, and defensive exposures while preparing for slower nominal growth and higher equity risk premia.

Q: How does demographic divergence affect geographic allocation?

A: Demographic divergence affects geographic allocation by favoring younger, faster‑growing regions for growth exposure and cautioning on very old populations with fiscal strain—migration policy can materially alter country outlooks.

Q: How do I incorporate demographic forecasts into portfolio construction?

A: Incorporate demographic forecasts into portfolio construction by layering scenarios (mild/moderate/severe aging), stress testing growth and real‑rate ranges, and adjusting strategic weights and glidepaths accordingly.

Q: What sample allocation shifts suit different investor life stages?

A: Sample allocation shifts for life stages: Accumulator 70–85% growth; Pre‑retiree 50–65% growth with higher liquidity; Retiree 30–50% income focus and 3–5 years liquid buffer; institutions extend duration and inflation hedges.

Q: What monitoring cadence and triggers should investors use for demographic risks?

A: Use a monitoring cadence tied to major releases (census, UN) and triggers like dependency ratio ±2 percentage points, cohort forecast ±5% over five years, and policy shifts in migration or retirement age.